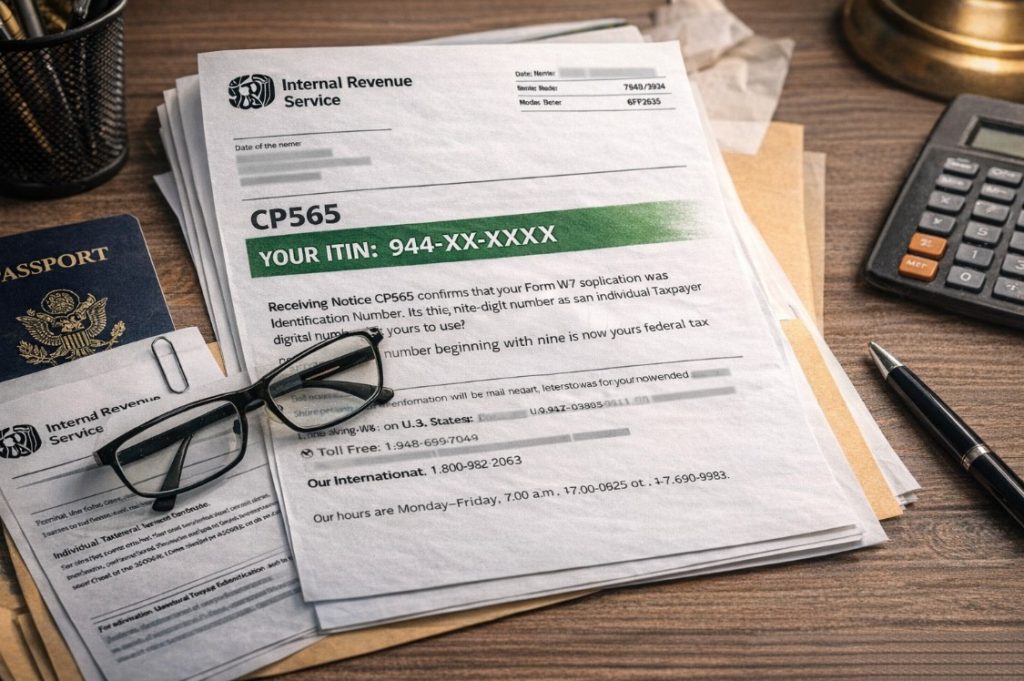

IRS Notice CP565 confirms your ITIN application was approved and provides your assigned number for tax filing purposes. Notice CP566 means the IRS needs additional documents within 45 days, while CP567 indicates your application was denied, but you can typically reapply.

After you submit Form W-7 to request an Individual Taxpayer Identification Number, the IRS reviews your application and sends an official written response. This response arrives as a standard notice informing you about your application status and any required next steps you must take going forward.

The notice you receive depends on how the IRS evaluated your documents, your eligibility, and whether your application was complete and accurate. Missing a deadline or misunderstanding instructions on these notices can result in denied applications, delayed refunds, or starting over completely from scratch.

If you want to learn more about what an ITIN is, that background knowledge will help you better understand these notices and their requirements.

This guide focuses on three IRS notices that ITIN applicants receive most frequently after submitting their W-7 application to the Internal Revenue Service offices. CP565 is the approval notice, CP566 requests additional information within 45 days, and CP567 indicates your application was denied for reasons listed.

You will typically receive one of these notices within seven to eleven weeks after the IRS receives your complete W-7 application package. Knowing what each notice means before you receive one puts you in a better position to respond quickly and correctly when that letter arrives.

Look at the notice number in the upper right corner of your IRS letter to identify which type of correspondence you received. The format will show CP565, CP566, or CP567 along with the date and your reference number for tracking purposes.

If you received CP565, the IRS approved your application and assigned you an Individual Taxpayer Identification Number for US income tax purposes. CP566 means your application is pending but requires additional documents within 45 days, as specified on the notice.

CP567 indicates the IRS reviewed your application and determined it could not be approved for specific reasons detailed in your letter. Most applicants can reapply after fixing the issues the IRS identified in their notice.

Receiving Notice CP565 confirms that your Form W-7 application was successfully processed and the IRS has assigned you an Individual Taxpayer Identification Number. This nine-digit number beginning with nine is now yours to use exclusively for federal tax filing purposes going forward.

The CP565 notice represents the successful completion of your ITIN application process, meaning the IRS verified your identity and accepted your reason for needing it. This approval typically arrives within seven to eleven weeks after the IRS receives a complete W-7 application with all required documents.

Your ITIN remains valid as long as you use it on at least one federal tax return during any consecutive three-year period. If the ITIN expires due to non-use, you can apply for renewal using Form W-7 with the appropriate renewal reason box checked.

Record your ITIN in a secure location where you can easily access it when preparing your federal tax return each year. Use your new ITIN on your federal tax return in the space designated for Social Security Number or ITIN, as applicable.

Do not use your ITIN for any purpose other than federal tax matters because it does not serve as valid identification otherwise. If you submitted a tax return along with your W-7, check your refund status because the IRS can now process your return.

Applicants often wonder how long they should expect to wait between submitting their W-7 and receiving their CP565 approval notice. If your name appears misspelled on the CP565, contact the IRS immediately using the phone number on your notice to request a correction.

More questions about ITINs are answered on the ITIN FAQ page that addresses common concerns from applicants.

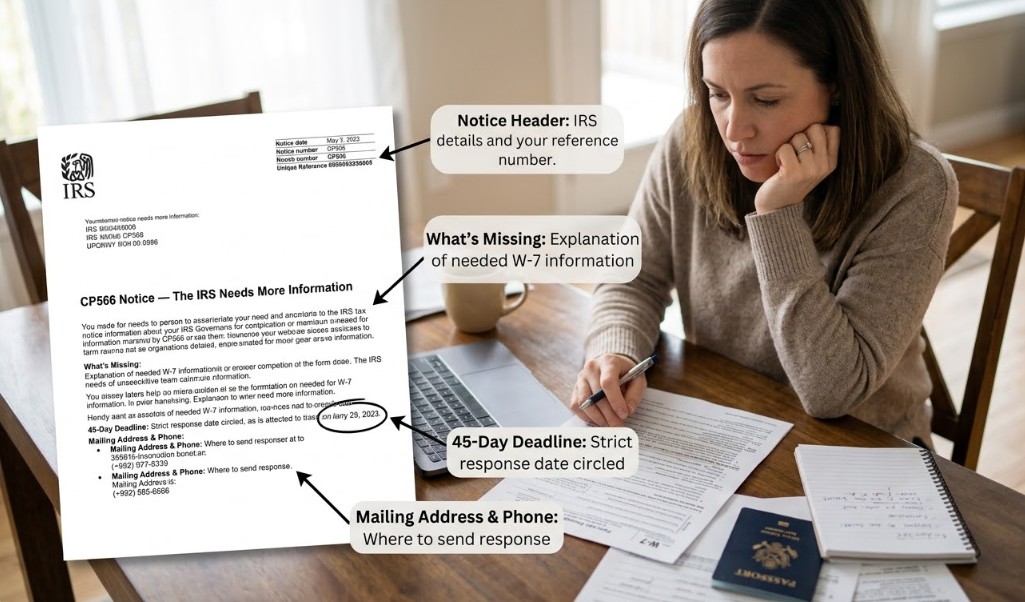

Notice CP566 indicates the IRS reviewed your W-7 application, but cannot complete processing without additional documentation or clarification from you. This notice is not a rejection but rather a request for more details before the IRS can make a final determination on your application.

The 45-day response deadline printed on your CP566 is strict, and failing to respond within this timeframe results in automatic denial. Many applicants feel anxious when receiving CP566, but most situations can be resolved by providing what the IRS specifically requested.

Missing or incomplete supporting documents represent the most frequent reason applicants receive CP566 notices from the IRS after submitting their W-7 applications. Document copies that fail to meet IRS certification standards often trigger these notices because the IRS requires specific types of document authentication.

Incomplete Form W-7 fields cause CP566 notices when applicants leave required boxes blank or provide information not match the instructions properly. Inconsistent information between your W-7 form and your supporting documents also triggers these requests when the IRS cannot reconcile the differences.

Read your CP566 notice carefully multiple times to fully understand exactly what documents or information the IRS is requesting from you specifically. Gather the requested documents using the exact format the IRS requires, whether certified copies, originals, or notarized translations of foreign-language materials for submission.

Write a brief cover letter including your name, your ITIN reference number from the notice, and a clear list of all enclosed documents. Include all required documents the first time you respond to avoid additional delays in your application processing timeline.

If you need assistance, a Certifying Acceptance Agent like Easy Tax Store can help you respond to IRS notices and prepare proper documentation.

Missing the CP566 response deadline results in automatic denial of your ITIN application, converting your pending status into a CP567 rejection notice. If you realize you cannot meet the deadline, call the IRS immediately using the phone number on your notice to request an extension.

Once denied due to a missed deadline, you must start the entire ITIN application process over from the beginning with a new Form W-7. Document any extension request by writing down the date you called, the representative's name, and any confirmation number they provide you.

Receiving Notice CP567 means the IRS reviewed your Form W-7 application and determined it cannot be approved based on the information and documents submitted. The notice specifies exactly why your application was rejected, so you understand what went wrong.

A CP567 rejection does not permanently bar you from obtaining an ITIN if you address the issues identified and submit a new application. Review your notice carefully to understand the exact rejection reason before deciding whether to reapply or seek professional assistance.

| Rejection Reason | What It Means | How to Fix It on Reapplication |

|---|---|---|

| Incomplete/missing documents | Required documents were not included | Submit all required documents in certified format |

| The applicant does not meet the eligibility requirements | You may not qualify for an ITIN | Review eligibility requirements before reapplying |

| Expired supporting documents | Identity documents were past their valid date | Obtain current, unexpired documents first |

| Failure to respond to CP566 | You missed the 45-day deadline | Submit a complete application with all items |

| Duplicate ITIN on file | Records show you already have an ITIN | Contact the IRS; you may need a renewal instead |

| Tax return not attached | The required return was not included | Include the federal tax return with the new W-7 |

| Inconsistent information | Details on W-7 do not match documents | Verify that all information matches exactly |

Yes, you can reapply for an ITIN after receiving CP567 in most circumstances once you address the specific issue that caused the denial. There is no waiting period between receiving a rejection and submitting a new W-7 application with proper documentation.

Fix the exact problem identified in your notice before submitting to avoid receiving another rejection for the same reason. Consider using a Certifying Acceptance Agent for your reapplication to ensure documents meet IRS requirements.

If you believe your application was incorrectly rejected and you have evidence supporting your position, you may have options to dispute the decision. Appealing makes sense when you submitted all the required documents correctly, but the IRS misread or overlooked something.

If the rejection was based on genuinely missing or incorrect information, reapplying with corrections is usually faster than appealing.

Look at the upper right corner of your IRS letter, where the notice number appears prominently near the date and your reference information. Check the date because this affects any deadlines, particularly the 45-day CP566 response requirement that runs from the issue date.

CP565 delivers good news about approval, CP566 requests additional information with a deadline, and CP567 explains rejection. If your notice is damaged or illegible, call the IRS using the general ITIN inquiries phone line for assistance.

Double-check every field on Form W-7 before submission to ensure you completed all required sections accurately and legibly. Use original documents or properly certified copies rather than regular photocopies because the IRS has specific authentication requirements for identity verification.

Include every required supporting document with your initial application to avoid receiving a CP566 notice requesting items you should have submitted. Check the tax forms instructions for detailed requirements about acceptable document formats.

Consider applying through a Certifying Acceptance Agent who can review your application for completeness and verify your identity documents. Keep copies of your entire application package and file early in the season to allow adequate processing time.

Ignoring CP566 and letting the 45-day deadline pass without responding is the most damaging mistake because it automatically converts your pending application to denial. Sending documents to the wrong IRS address causes delays and may result in lost materials never connected to your application.

Forgetting to include the notice reference number makes it difficult for the IRS to connect your documents to your application file. Assuming CP567 means you can never obtain an ITIN is incorrect because most rejections can be resolved by fixing identified problems and reapplying.

Notice CP565 confirms the IRS approved your Form W-7 application and assigned you an Individual Taxpayer Identification Number for federal tax purposes. Your ITIN appears on the notice for you to record securely for use on future tax returns and tax-related documents.

You have 45 days from the date on your CP566 notice to submit the requested documents or information before the IRS denies your application. If you need additional time, contact the IRS immediately using the phone number on your notice to request an extension before the expiration.

Yes, you can reapply for an ITIN after receiving a rejection notice by submitting a new Form W-7 with corrected information and proper documentation. There is no waiting period, but address the specific rejection reason stated in your CP567 notice before reapplying again.

Common CP566 requests include certified identity documents such as passports, missing proof of foreign status, additional documentation supporting your reason for needing an ITIN, or clarification about inconsistent information between your Form W-7 and supporting materials submitted.

Current IRS processing times for ITIN applications range from seven to eleven weeks for complete applications submitted with all required documentation included. Processing may take longer during peak tax season from January through April when the IRS handles higher application volumes.

Contact the IRS directly to request your ITIN number or obtain a replacement notice confirming your assigned number for your records. You can also find your ITIN on previously filed tax returns if you used it after receiving your original CP565 approval notice.

Easy Tax Store operates as an IRS-authorized Certifying Acceptance Agent, helping ITIN applicants respond to CP566 requests and prepare stronger reapplications after CP567 rejections. Our team reviews documents for completeness and verifies they meet IRS requirements. Contact our ITIN services team, get a free tax estimate, or contact us directly.